Similarweb 2026 Generative AI Visibility Index

Similarweb recently published its 2026 Generative AI Brand Visibility Index report, which offers rich insights into the evolving roles that generative AI platforms like ChatGPT play in people’s purchase decisions.

In this article, Chase Buckle and Simon Kemp offer DataReportal’s independent analysis and perspectives on Similarweb’s report, by:

Unpacking the report’s key takeaways;

Offering additional perspectives and conclusions; and

Suggesting next steps for marketers and digital practitioners.

Notes on terminology

Throughout this analysis, we’ll refer to platforms like ChatGPT, Gemini, Claude, and Perplexity as “GenAI” (i.e. generative AI) platforms. These platforms primarily use underlying large language models (LLMs) and artificial intelligence technologies (AI) to generate outputs for users, so we use the umbrella term “GenAI” to refer to these platforms’ user-facing services.

Executive summary

Top takeaways

Similarweb’s report offers three primary conclusions:

A few brands tend to dominate AI mentions, but visibility is volatile.

Within each category, a small number of brands capture a disproportionate share of GenAI visibility. However, even top performers can see their visibility fluctuate dramatically from month to month.Some challenger brands are accelerating their GenAI visibility.

Despite the dominance of large brands, some smaller brands punch above their weight in GenAI visibility, while other brands appear to struggle, despite strong consumer recognition.Specialist and information-led brands outperform.

In every sector, specialist or education-led brands rank significantly higher in GenAI visibility than their performance in branded search demand might suggest. This is not incidental, and reflects a fundamental about how GenAI systems select and synthesise information.

Similarweb’s findings point towards an important shift in competitive advantage that marketers need to be aware of, as Similarweb’s analysts note:

“[GenAI] is increasingly shaping how consumers discover brands, evaluate options, and form purchase intent. Visibility is no longer defined by a ranking position, but by inclusion within the [GenAI] conversation.”

So what must marketers do to capitalise on the growing opportunities within GenAI platforms like ChatGPT?

Let’s start by quantifying the current scale of global AI use, before looking at where AI might fit in the marketing mix, and how we can maximise its value.

Putting GenAI adoption in context: 2 billion users

It’s barely been 40 months since ChatGPT burst onto the scene in November 2022, but since then, GenAI platforms have taken the world by storm.

Our analysis of data from a variety of different sources indicates that there are now well over 2 billion active users of GenAI platforms like OpenAI’s ChatGPT, Google’s Gemini, and Anthropic’s Claude.

We’re aware that reports of AI use often tend towards hyperbole though, so – for reassurance and transparency – here’s how we arrived at that number.

In late February 2026, OpenAI published a blog post stating that ChatGPT has more than 900 million weekly active users (WAU).

Meanwhile, our analysis of Similarweb data profiling worldwide use of ChatGPT’s mobile app between August 2025 and January 2026 indicates that the ratio of monthly to weekly active users (MAU vs WAU) is 1.32. If we apply this ratio to OpenAI’s WAU figure, Similarweb’s data suggests that ChatGPT’s MAU total currently stands at roughly 1.19 billion.

Furthermore, our analysis of Similarweb data profiling traffic to a selection of the world’s most popular GenAI websites indicates that roughly 1 in 4 active GenAI web users outside of mainland China do not visit ChatGPT’s website, suggesting that the total number of GenAI users outside of China now exceeds 1.57 billion.

But we also need to add figures for users living inside China’s Great Firewall. According to CNNIC’s 57th Statistical Report (in Mandarin) on internet use within the country, there were already 602 million GenAI users in mainland China in December 2025.

And once we add this to our “rest of world” total, we arrive at a global active GenAI user figure of 2.17 billion.

For perspective, that figure equates to more than 1 in 4 people on Earth, suggesting that over a quarter of the world’s total population may already use GenAI every month.

So, there’s little doubt that GenAI platforms already offer compelling opportunities for brands.

However, as we’ll explore in more detail below, the determinants of marketing success on these platforms are already evolving.

Understanding GenAI’s role in the purchase journey

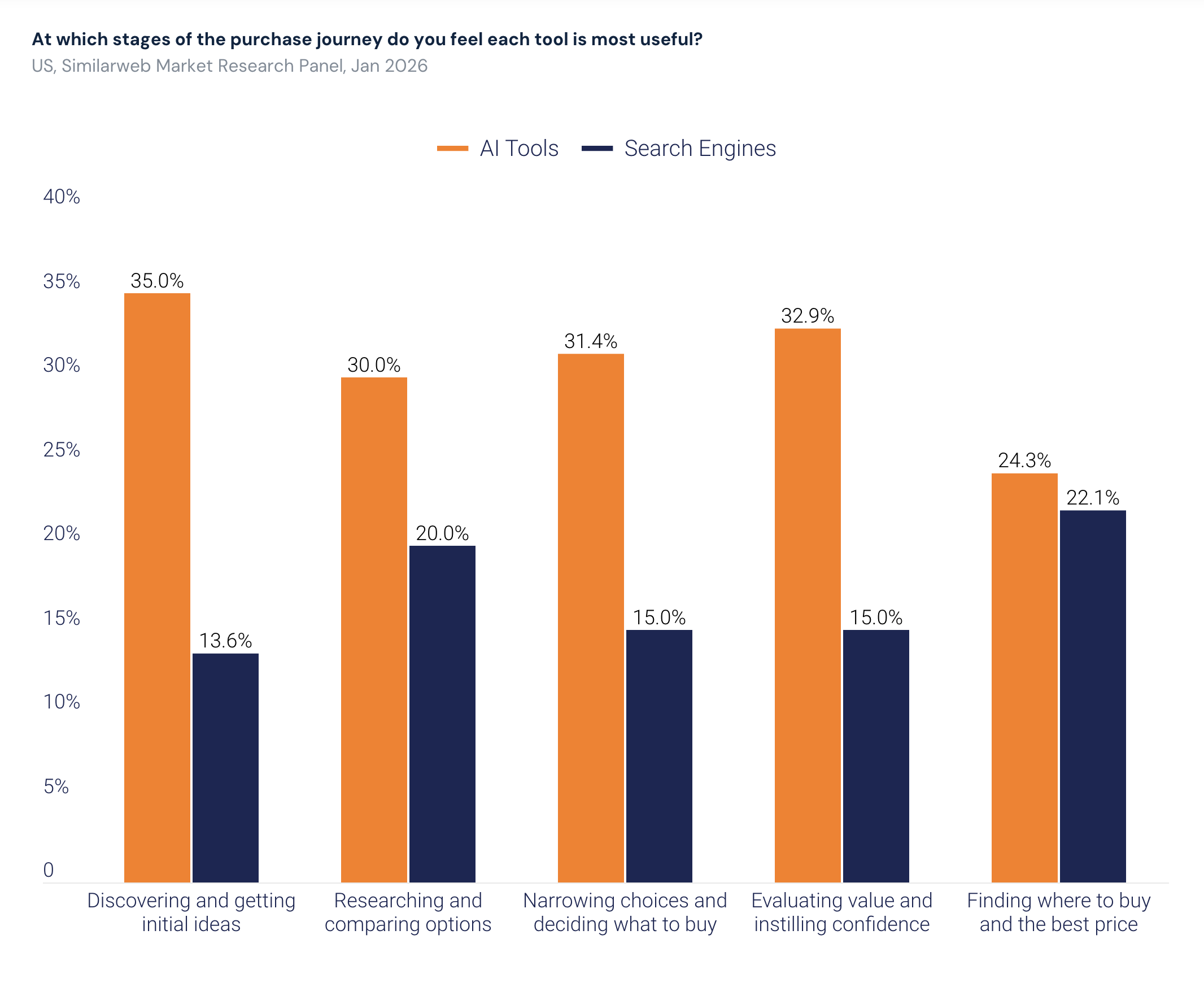

Similarweb’s Market Research Panel data among US consumers gives us a clear picture of where consumers believe GenAI is most useful across various stages of the buyer journey.

Notably, Similarweb’s data indicates that American consumers find AI tools most useful during the initial stages of a purchase cycle, when they’re looking for initial ideas.

And in fact, more than 1 in 3 survey respondents (35%) say that they use AI tools during this discovery stage.

However, at least 3 in 10 say that they turn to AI tools to research options and compare alternatives too, with respondents to this particular survey indicating that AI tools may be even more useful than search engines for each of these activities.

Digging deeper into Similarweb’s findings

In addition to the conclusions outlined in our executive summary, Similarweb’s report offers another, somewhat profound takeaway: GenAI platforms already appear to be reducing the rate at which they refer visitor traffic to third-party websites.

For context, Similarweb’s data indicates that the absolute volume of GenAI referrals continued to grow until the last quarter of 2025, but over the past few months, total outbound clicks have been declining steadily. Similarweb’s analysis indicates that GenAI platforms referred 226.8 million US visitors to third-party sites in January 2026, which is a full 15% less than the 267.4 million that the same platforms referred to third-party web domains in October 2025.

And this decline becomes even more apparent when we measure the “referral rate” – i.e. the number of outbound clicks to third-party domains, as a percentage of total visits to GenAI platforms. For example, in the United States, the referral rate dropped from 18.8% in October 2025 to 15.8% in January 2026. This 2.4 percentage-point drop equates to a relative decline of 16.4%, which in turn represents the loss of roughly 1 in every 6 outbound clicks in the space of just three months.

What this means for measuring AI marketing

In their report, Similarweb’s analysts note that this trend is likely symptomatic of a move by GenAI platforms to offer “all-in-one” solutions, where users are increasingly – and intentionally – kept within the platform. Marketers should note that this approach would be nothing new though; social media platforms set a clear precedent for such practices when they reduced the algorithmic prominence of third-party (i.e. outbound) links in the early 2010s.

Moreover – and perhaps more importantly – we’ve identified compelling evidence to suggest that search engines like Google are also taking more proactive steps to keep traffic within their platforms, as we saw in our recent analysis of Wikipedia traffic (also using Similarweb data).

And the clear takeaway for marketers here is that, increasingly, outbound clicks and referral traffic will not provide a representative measure of the role that GenAI platforms play within people’s overall purchase journeys, nor of the role that they play within the broader marketing mix.

Consequently, Similarweb’s analysts suggest that brand visibility should become the primary metric for measuring marketing performance within GenAI platforms like ChatGPT.

GenAI measures of success

Chase’s analysis

When it comes to measuring AI’s value to marketers, referral traffic was always going to be a distraction, because the real influence of GenAI interfaces and outputs on people’s brand choices cannot be reduced to mere clicks.

But it’s worth making another important distinction here too. Similarweb’s panel data measures something more specific than usage: usefulness. These two things are very different, but they’re also complementary, and Similarweb’s report makes it clear that consumers have already embraced GenAI for useful discovery and research. Indeed, data suggests that these tools have already become well established in consumers’ mindsets and behaviours.

And taken together with the referral traffic trends we explored above, this finding offers further insight into how AI influence actually operates. More specifically, the decline in outbound referral rates reveals how influence is evolving within AI interactions: users are asking questions, weighing options, comparing brands, and even reaching conclusions, often without ever clicking on any external links.

In other words, GenAI influence often occurs before a potential buyer goes anywhere else, and before they do anything beyond the AI platform. And crucially, that means GenAI’s influence is concentrated in the initial thinking phase of the purchase journey, upstream of most other marketing channels.

Consequently, the most important question for marketers is not how much traffic AI sends to their websites, but rather, whether their brands appear clearly and credibly within the AI interactions that inform shoppers’ initial thinking phases.

And that is exactly what Similarweb’s Visibility Index sets out to measure. But what does their valuable study tell us about the current state of GenAI marketing?

Visibility, concentration, and volatility

Simon’s analysis

Firstly, Similarweb’s report offers fascinating insights into how volatile GenAI mentions can be, with the visibility of some brands fluctuating dramatically over time, often without obvious explanation.

For example, despite being one of the most visible brands in the Financial Services category, Nerdwallet saw its AI Visibility Index score swing by more than 100% during the reporting period, from a low of 77, to a high of 151. Moreover, those two extremes were only three months apart.

Meanwhile, in the Fashion category, Macy’s experienced even more dramatic movement, with its Index score jumping from 119 to 326, and then back to 158 – all within the space of just five months.

It’s important to note that Similarweb identified both of these brands as “accelerating” their GenAI visibility during the study period, so the volatility in their respective scores doesn’t indicate any underperformance by either brand. However, given that even top-performers experience big swings in visibility, it’s reasonable to conclude that optimising for AI visibility won’t be a “set-and-forget” activity. Indeed, our primary takeaway from these two examples is that maintaining GenAI visibility may be just as hard as achieving it in the first place.

Having said that though, Similarweb’s data also indicates that some of the most visible brands manage to avoid such volatility. For example, Apple tops the Consumer Electronics category by a considerable margin, with the brand’s overall Visibility Index score (100) more than four times higher than that of its next nearest rival, Samsung (24). But perhaps more importantly, Apple’s Visibility Index also remained far more stable than some of the other brands in this category, and its monthly score only moved between 87 and 105 over the course of the reporting period. Meanwhile, Nike tops the Fashion category with similarly low volatility, and Nike’s Visibility Index score only ranged between 91 and 101 during the study period.

Crucially, our analysis of brands that maintain stable positions versus those that experience more dramatic swings reveals one of the most instructive patterns in the data. In particular, top performing brands tend to be those with the most established and widespread presences across information ecosystems outside of AI, and this in turn may help explain why GenAI visibility is so concentrated amongst a relatively small group of brands. This finding might suggest that making it to the top of the rankings could be especially difficult for smaller and less established brands, but – as we’ll see below when we come to our “redefining competitive advantage” section – data suggests that this challenge is not an insurmountable one.

Chase’s perspective:

The volatile nature of GenAI visibility revealed in Similarweb’s report is striking, as is the concentration of brands that manage to show up in results. But it’s worth asking ourselves a more fundamental question when we’re exploring these results: are they what we expect?

Understanding structural reasons is just as important as tracking the individual swings in visibility. And the answer lies in something surprisingly simple: the number of inventory slots available.

When a search engine results page surfaces ten brands, a brand dropping from position three to five loses some exposure, but stays visible. The inventory of slots available is large enough to absorb movement without catastrophic consequences. But when a GenAI response surfaces three brands, the same scenario doesn’t produce a gradual decline, it produces a cliff edge in visibility for that brand: it’s either in the response or it’s not. If it’s not, its visibility drops to zero.

Let’s think about what that means in practice by cross-referencing Similarweb’s data with data from GWI. GWI data puts the use of search engines for brand discovery at around one-third of online consumers globally, while GenAI sits at less than half that figure: 14.8%.

But that user gap is only part of the story. Let’s assume that search engines surface ten brands in their results, and that GenAI platforms surface three. Put those two things together — fewer users, fewer slots per interaction — and some crude back-of-napkin maths tell us that AI generates roughly eight times fewer brand visibility moments than search engines. And that’s before factoring in interaction frequency. Consumers are likely running far more brand discovery-related searches per day than they are GenAI queries, which would push that gap wider still.

This is why the volatility we see in Similarweb’s GenAI visibility data isn’t surprising, and also why it isn’t going away. This is unlikely to be a teething problem that will smooth out as GenAI matures. It’s a structural artefact resulting from how GenAI compresses brand visibility in its answers. Fewer slots mean even a small change in how an AI model weights its sources can produce very large swings in brand exposure in short periods of time.

The same logic also explains Similarweb’s findings of strong concentration in the number of brands that tend to get surfaced, especially in industries like Fashion and Consumer Electronics. Fewer slots available than search, many brands competing for them, more visits to search engines than GenAI tools, and the result is a power-law distribution: a small number of brands capturing a disproportionate share of whatever visibility inventory exists.

Redefining competitive advantage

Simon’s take

While brand concentration and “visibility volatility” are clearly features of GenAI visibility today, Similarweb’s report also offers compelling evidence that – with the right approach – brands of all sizes can still compete.

Indeed, across every product category featured in Similarweb’s report, there are various examples of brands that “outperform” in AI visibility compared with their performance in areas such as branded search engine queries or market position.

For example, in the Financial Services category, information-led brands and comparison platforms rank well above their branded search demand. Similarly, in the Consumer Electronics sector, specialist and review-led sources often appear alongside – or even ahead of – established retail brands. And furthermore, these same dynamics reappear across Fashion, Travel, Beauty, and News.

Similarweb’s Director of Product Marketing, Adelle Kehoe, offers valuable insight into the drivers of this trend:

“AI search represents an opportunity for all, not just a playground for incumbents. Rising players tend to share common traits: high-quality, specialist content, and deep subject-matter expertise.”

And Adelle concludes her analysis with one of the most important takeaways in the whole report:

“Authority, not just scale, is emerging as the differentiator.”

Chase’s take

Similarweb’s emphasis on authority indicates that while things like brand popularity, market share, and advertising spend can feed into the conditions that make a brand more likely to appear in a GenAI response, these do not appear to be the measures that GenAI platforms themselves are optimising for. Building a strong brand matters and clearly pays off in GenAI visibility, but it operates on a long-term horizon, and doesn’t fit neatly into a playbook for more immediate results.

What Similarweb’s “overachiever” finding gives us is something that does. GenAI platforms select sources that best answer the question being asked; completely, credibly, and clearly. The brands that overachieve in GenAI visibility are the ones that have, often without intending to, built their entire content model around doing exactly that. They produce structured, neutral, genuinely useful information. They answer the questions that consumers actually ask.

Building brand salience in GenAI

Simon’s perspective

Reassuringly, these findings suggest that marketers don’t need to craft specialist, standalone marketing programmes in order to improve their brand’s salience in GenAI answers. Indeed, Similarweb’s data indicates that GenAI visibility often depends on the very same factors that determine brand awareness, consideration, and intent amongst humans.

Crucially, the available research indicates that direct query relevance is the primary factor that LLMs use to determine which brands to cite or reference in their answers. Moreover, that relevance is shaped by contextual evidence.

But where do GenAI platforms source their evidence? In all honesty, that’s still something of a “black box”, and neither human developers nor the tools themselves seem to be able to offer a comprehensive answer.

However, we’ve seen credible evidence to suggest that some of the more “established” marketing channels also feature prominently when it comes to influencing GenAI brand visibility, notably brand websites, social media mentions, and classical PR.

Brand websites and GenAI answers

In DataReportal’s own studies, GenAI answers regularly reference and cite content sourced from brands’ own web properties. As a result, marketers should strive to include all of the information that they’d hope to see within AI answers somewhere on their own website(s).

Marketers should also ensure that it is easy for LLM crawlers and AI bots to find, categorise, and process that content. For example, AI systems will require significantly fewer resources to process text content than they will to analyse and transcribe a video.

Social media influences AI conversations

Our studies indicate that “authoritative” third-party perspectives also play an important role in shaping GenAI visibility. For example, Google has publicly indicated that it places significant emphasis on “expert”, human opinions shared on social media forums like Reddit.

As such, marketers may want to re-elevate the emphasis they put on inspiring organic social media mentions and collaborating with credible influencers. It may also be worth re-exploring the topics that brands publish to their own social media channels, because these will likely play an equally important role in “feeding” GenAI answers.

Public relations shape machine relations

When asked via their own chatbots, various GenAI platforms – including ChatGPT, Gemini, and Claude – indicate that they place particular significance on content sourced from “authoritative” news media, with outlets such as the BBC, the New York Times, Reuters, and the Financial Times offered as examples.

Consequently, classical PR has a powerful role to play in boosting GenAI visibility too. For clarity, it’s important to stress that marketers and PR professionals will want to focus on using such activities to build and reinforce the contextual relevance of their brand to specific consumer needs and situations, beyond merely attracting “media mentions”.

However, it’s also worth highlighting that DataReportal’s own qualitative (and admittedly somewhat crude) analysis indicates that “paid” PR partnerships can be just as effective as organic mentions. Similarly, offering journalists the opportunity to interact more extensively with senior executives can deliver meaningful results when it comes to building B2B and investor brand visibility via GenAI.

Chase’s analysis

The reason these fundamentals matter comes down to a simple dynamic. GenAI doesn’t show consumers your brand; it decides first whether your brand deserves to be in the answer by looking for evidence. To reach the human, you first need to be legible to the machine that determines what the human sees. Crucially however, that machine legibility is built from exactly the same kinds of credibility factors which matter to humans.

At its core, everything we’ve just explored is classical brand building. What’s perhaps most ironic about GenAI visibility is its implications for the brand-building versus performance marketing debate.

While both are crucial to sustainable business growth, many companies have found it easier to justify short term marketing tactics due to the perceived benefits of seeing investment returns and attribution. But now, if a brand wants to “pay to play” in the AI visibility competition, the methods for doing so cannot be bought quickly or manufactured. They require constant investment and a tolerance for investing in something which, by design, does not have immediate and clearly attributable results to show to the board on a tidy chart.

When viewed from another perspective, this also cements the need for market research as a means of priming a brand for better GenAI visibility. And this relates directly to the finding that specialist and information-led brands often “outperform” when it comes to AI visibility.

To over-simplify: GenAI answers are constructed word-by-word, based on the probability of what the next word should be, thanks to all the information ingested to deliver that answer. That means GenAI is essentially trying to answer the question a consumer is asking about a brand as completely and reliably as possible. In doing so, the brands and sources these tools draw from are the ones that have already done that job well via the combination of sources detailed above. These are the brands highlighted by Similarweb that are “overachieving” in GenAI visibility.

Brands wanting better AI visibility need to invest in more practically understanding their customer base:

Who these people are

What they need to know to make a decision

How and why they would buy your product, and the blockers that prevent purchase

The information that resolves those blockers

The comparisons people need to feel confident

Content that maps to these needs, and produces genuinely useful answers, is building GenAI visibility as a byproduct of information authority. As a result, knowing your customer more intimately than your competitors is not just a nicety, nor a concept that can be parroted with no substance. It’s something which delivers proven advantage in how consumers are increasingly deciding which brands to feature in their consideration set.

Chase’s parting thought: the quiet upside of GenAI visibility

The conversation around GenAI in marketing often focuses on what brands stand to lose. These concerns are legitimate; GenAI is undermining some of the familiar metrics that have defined digital performance for decades, and its unrelenting advance in adoption and capabilities can leave us feeling like we’re losing control.

But the data in Similarweb’s report points to something that is both positive and worthy of wider discussion: the incentive structure that GenAI visibility is quietly creating is, in many respects, a healthy one.

Brands that create content that is genuinely useful, credible, and well-structured are rewarded by GenAI. Taking the time to understand customers’ real needs and questions, and answering them honestly, will work in a brand’s favour. This gives valuable credence to the arguments espousing the importance of brand building as well as performance marketing. And crucially, it gives brands of any size a productive path to visibility, underpinned by quality and authority rather than the size of your budget.

In other words, to perform well in GenAI, brands have to actually be good at the things marketing has always claimed to care about: knowing the customer, building genuine credibility, and producing content that earns trust rather than just attention.

The concentration of, and volatility in, GenAI visibility are real challenges. The opacity of measurement is also frustrating, as is the AI slop filling our newsfeeds.

But if GenAI creates a durable incentive for brands to invest in real customer-centricity, and in the marketing principles that have driven the most enduring brands for generations, that might be one of the industry’s most positive developments in a long time. And it’s one that still seems to fly under the radar.

Learn more

Dig deeper into Similarweb’s complete 2026 Generative AI Brand Visibility Index report, and find GenAI visibility scores for a number of different brands, by clicking here.

Disclosures

Similarweb is one of DataReportal’s primary research partners. However, this article represents DataReportal’s independent analysis of Similarweb’s report and data, and neither DataReportal, its analysts, nor its owners received financial compensation from Similarweb for the production or publication of this article.

Click here to see all of Chase’s articles, read his bio, and connect with him on social media.

Click here to see all of Simon’s articles, read his bio, and connect with him on social media.